Building a fintech product with a development agency costs $80,000 to $250,000 and takes six to twelve months before a single user can validate the idea. Most fintech founders with a genuine problem to solve cannot justify that bet before confirming market demand. According to CB Insights, 38% of fintech startups fail because they run out of capital before reaching product-market fit (CB Insights, 2023), and the largest single draw on that capital in the early stage is premature technical hiring. AI-generation tools have changed the math. A full-stack fintech MVP, with dashboards, user authentication, payment flows, and role-based data access, now generates from a plain English description in days. This article covers seven specific ways fintech founders are building and launching apps without developers in 2026. For the broader framework of building a tech startup without a developer, this guide on how to build a tech startup without a developer covers the full workflow from idea to deployed product.

TL;DR Fintech founders are launching payment dashboards, lending MVPs, expense trackers, subscription billing tools, CRM systems, investor portals, and compliance-ready internal tools without developers using imagine.bo’s Describe-to-Build interface. The platform generates a full-stack application from plain English, starting at $0. According to Stripe, 87% of SaaS and fintech companies that ship an MVP within 90 days of starting development reach their first $10,000 MRR faster than those that wait longer (Stripe, 2023). Custom builds on imagine.bo cost under $350 in year one versus $80,000 to $250,000 from a development agency.

Way 1: Payment Dashboard MVPs

The most common first fintech product is a payment or transaction dashboard: a tool that aggregates transaction data, surfaces key metrics, and gives users visibility into their financial activity that their bank’s interface does not provide. According to McKinsey, 65% of consumers report using at least one fintech app specifically because it surfaces financial data more clearly than their primary bank (McKinsey, 2024).

Launch Your App Today

Ready to launch? Skip the tech stress. Describe, Build, Launch in three simple steps.

Buildimagine.bo generates a complete payment dashboard from a description, including the transaction data model, the metrics calculations, the filtering and search interface, and the role-based access for different user tiers. A strong starting prompt names the transaction fields, the aggregation metrics, the user roles, and the access rules explicitly. “Build a payment analytics dashboard for small business owners. Each user connects their Stripe account. The dashboard shows total revenue this month, last month, and year to date. It shows a transaction list with date, amount, customer name, status, and payment method. Users can filter by date range, status, and payment method. Admin users can see all user accounts and their metrics. Standard users can only see their own data.”

The Stripe account connection and the OAuth flow for linking user accounts are tasks for the Hire a Human feature at $25 per page, since OAuth token management requires precise implementation. Everything else, the dashboard metrics, the filtering, the role separation, generates correctly from the prompt. For the common integration errors that arise when connecting payment data to custom dashboards, this post on common Stripe payment integration challenges covers the architectural decisions that prevent silent failures.

Way 2: Lending and Credit MVPs for Validation

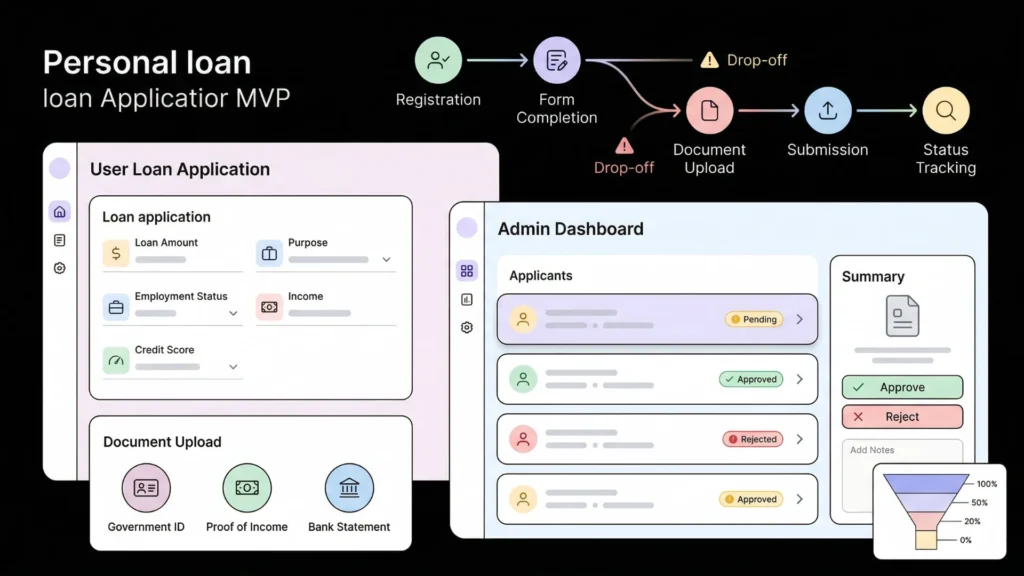

Fintech founders building lending products need an MVP that validates the application flow, the underwriting criteria, and the user experience before writing a single line of custom risk logic. A custom lending application built on imagine.bo handles the loan application form, the document upload workflow, the admin review interface, and the approval or rejection notification flow. That is enough to put real applicants through the process and validate drop-off rates, document friction, and decision turnaround expectations before the product needs to connect to actual capital.

The most valuable thing a lending MVP validates is not whether users want loans. They do. It validates which step in the application flow loses the most applicants. A custom-built application with tracking on each form step reveals whether applicants abandon at document upload, at income verification, or at the waiting period after submission. Generic forms or survey tools cannot capture that sequential drop-off data. An imagine.bo-generated lending application captures it from the first applicant through the built-in analytics dashboard.

A lending MVP prompt: “Build a personal loan application platform. Applicants register, complete a loan application with requested amount, purpose, employment status, monthly income, and credit score range. Applicants upload three documents: government ID, proof of income, and bank statement. After submission, applicants see a status page showing pending review, approved, or rejected. Admins see all applications with status, can view submitted documents, and can approve or reject applications with a note. Rejected applicants receive an email with the reason. Approved applicants receive an email with next steps.”

For validation methodology before building, this guide on validating startup ideas with no-code tools covers how to confirm demand before investing in the full build.

Way 3: Subscription Billing and Recurring Revenue Tools

Fintech founders building B2B SaaS products with subscription billing need a billing management system that handles plan selection, payment processing, upgrade and downgrade flows, and invoice generation without a $400 per month billing platform. imagine.bo generates the complete subscription billing infrastructure from a description, and the subscription lifecycle webhook handler is the specific task where Hire a Human produces more reliable outcomes than prompt iteration alone.

According to Stripe, involuntary churn from failed subscription payments accounts for 20 to 40% of total SaaS churn (Stripe, 2024). A custom-built billing system with Stripe Smart Retries enabled and a dunning email sequence recovers a meaningful share of that churn at zero incremental cost beyond the initial build.

A billing tool prompt: “Build a subscription billing platform for a B2B SaaS product. Users select a plan at signup: Starter at $29 per month, Growth at $79 per month, and Scale at $199 per month. Each plan has feature limits shown on a pricing page. Users enter payment details via Stripe Checkout. The billing dashboard shows current plan, next billing date, payment history, and a downloadable invoice for each payment. Users can upgrade their plan immediately and downgrade at end of cycle. Admins see all subscribers, their plan, payment status, and monthly recurring revenue total.”

For the full subscription architecture including webhook handling for lifecycle events, this guide on launching a subscription-based app without developers covers the implementation in detail.

Way 4: Expense Tracking and Budget Management Apps

Business expense tracking is a fintech category where every existing tool either costs too much for small teams or does too little for growing ones. A custom expense tracker built on imagine.bo matches the specific approval workflow, expense category structure, and reporting requirements of the exact business it is built for. Generic tools approximate that structure. A custom build implements it precisely.

The expense app prompt element that most affects generation quality is the approval workflow specification. “Employees submit expenses for approval” generates a generic two-step flow. “Employees submit expenses under $500 for direct manager approval. Expenses above $500 require manager approval followed by finance team approval. Expenses over $2,000 require a second finance approver. Rejected expenses return to the employee with a required reason.” That specification generates the multi-step approval state machine with the correct routing logic on the first generation.

For a practical guide to AI tools specifically in financial management contexts, this post on AI in finance and no-code tools for budgeting covers the fintech application landscape in more detail.

Way 5: CRM and Client Management for Financial Services

Financial advisers, insurance brokers, mortgage brokers, and wealth managers need CRM tools that track client relationships, financial product holdings, and compliance documentation in a structure that generic CRMs like HubSpot or Salesforce do not support natively without expensive customisation. A custom financial services CRM built on imagine.bo generates the exact data model, the exact pipeline stages, and the exact compliance documentation fields the specific business needs.

A financial adviser paying $150 per month for Salesforce Essentials plus $200 per month for a financial planning plugin spends $4,200 per year on CRM infrastructure that still requires manual workarounds for regulatory document tracking. A custom CRM built on imagine.bo’s Pro plan at $25 per month with the exact fields and workflows the adviser uses costs $300 in year one. The productivity gain from a tool that matches actual workflow rather than requiring adaptation to a generic structure is an additional benefit that compounds with every client added.

A financial CRM prompt: “Build a client management platform for a financial adviser. Each client record includes personal details, risk tolerance, investment objectives, and linked financial products with values and last review dates. Advisers can log client interactions with date, type, and notes. The dashboard shows clients due for annual review in the next 30 days and clients with compliance documents expiring in the next 60 days. Document storage allows uploading signed agreements, ID verification, and KYC documents per client. Admins can see all advisers’ client lists. Each adviser can only see their own clients.”

For a detailed guide to building a custom CRM without coding, this post on how to create a custom CRM app without coding walks through the data model and prompt structure.

Way 6: Investor and Cap Table Portals

Fintech founders raising capital need a portal where investors can view their investment details, access financial updates, sign documents, and review cap table information without the founder emailing spreadsheets and PDFs manually. A custom investor portal built on imagine.bo generates this infrastructure in a day. It replaces the manual communication overhead that consumes founder time at the exact moment investor confidence needs to be highest.

A compact but complete investor portal prompt: “Build an investor portal for a startup. Investors register via email invitation from the admin. Each investor sees their own investment amount, equity percentage, and investment date. The portal shows company updates posted by the admin with date and content. Investors can download quarterly reports uploaded by the admin as PDFs. The cap table section shows all investors, their share class, shares held, and percentage. Admin can see all investors, post updates, upload documents, and manage the cap table. Investors cannot see other investors’ personal contact details but can see their share holdings.”

Built-in RBAC and SSL on every imagine.bo deployment matter specifically for investor portals, where cap table data is sensitive and access control errors have legal implications. Review the access rules in the AI-Generated Blueprint explicitly before confirming the build. For the full security configuration checklist for AI-generated applications, this post on prompt-based app security best practices covers the audit approach.

Way 7: Internal Compliance and Operations Dashboards

Fintech companies handling regulated data need internal tools for tracking compliance tasks, audit logs, KYC document status, and regulatory deadline management. These tools are almost never available as off-the-shelf products because every regulated business has a slightly different compliance structure. They are also expensive to custom-build because compliance requirements make the brief complex. imagine.bo generates the data model and the workflow from a description, and the access control and audit logging defaults handle the baseline compliance requirements automatically.

Citation capsule: Every application generated on imagine.bo includes role-based access control enforced at the API layer, SSL on all deployments, data encryption in transit and at rest, and GDPR and SOC2 readiness foundations applied by default, without additional configuration from the builder (imagine.bo, 2026). These defaults make compliance-adjacent applications significantly faster to build correctly than on platforms where security features require manual configuration.

A compliance dashboard prompt: “Build an internal compliance tracking tool for a fintech company. Compliance tasks are created with a title, description, owner, deadline, regulatory framework, and status: pending, in progress, review, and complete. The dashboard shows tasks overdue and tasks due in the next seven days. Each task has an activity log showing every status change with the user who made it and the timestamp. Admins can assign tasks and view all tasks. Standard compliance team members can only see tasks assigned to them. The tool exports a compliance task report as CSV for monthly regulatory submissions.”

For building internal analytics dashboards specifically, this post on building internal analytics dashboards with AI prompts covers the data modelling and dashboard generation workflow.

FAQ

Can a non-technical fintech founder build these apps without any coding knowledge?

Yes. imagine.bo requires describing your financial product’s workflow clearly in plain English. Fintech founders who understand their regulatory requirements, their user access rules, and their data model better than any developer they could hire at this stage produce the most accurate first generations. According to Gartner, non-technical professionals now build more applications than trained developers at many organisations, driven by AI-generation tools that convert domain expertise into working software (Gartner, 2022). This post on non-technical founders building products covers what that process looks like in practice.

How does imagine.bo handle the security requirements fintech apps need?

Imagine.bo generates every application with SSL on all deployments, RBAC enforced at the API layer, data encryption in transit and at rest, and GDPR and SOC2 readiness foundations by default. These are applied automatically without additional configuration. For fintech-specific requirements like PCI DSS for payment handling, the Hire a Human feature provides a vetted engineer for specific compliance implementations. For a complete security checklist for no-code applications handling sensitive financial data, this guide on no-code app security best practices covers every layer.

What is the fastest fintech app type to build without developers?

Internal compliance dashboards and investor portals are typically the fastest because they have a small number of user types, no payment processing, and well-defined data structures. Both reach a first deployed version in under a day. Payment dashboards and subscription billing tools take two to three days including the Hire a Human task for payment integration. For the full cost comparison across developer-built, SaaS, and AI-generated approaches, the 2026 breakdown covers what each approach costs across different fintech product types.

Conclusion

Fintech founders who build custom apps without developers gain three advantages over those waiting for a technical co-founder or an agency quote. They validate faster, reaching real users before capital runs out. They build exactly the compliance structure, data model, and workflow their specific product needs rather than adapting to a generic platform’s constraints. And they own clean, exportable code that a developer can extend without rebuilding from scratch when the product scales past what prompts can handle alone.

imagine.bo’s free plan provides 10 credits to deploy a first version at zero cost. The Pro plan at $25 per month adds 150 rollover credits, private projects, and a one-hour expert pre-launch session. Start with the app that addresses your most immediate validation need, likely the payment dashboard or the lending MVP, and get it in front of real users this week. For the complete workflow of describing and deploying a fintech application from a single plain English prompt, this guide on building an app by describing it is the most direct next step.

Launch Your App Today

Ready to launch? Skip the tech stress. Describe, Build, Launch in three simple steps.

Build